Manage your own investments - It can be easy and well worth the effort.

Just 10 minutes on the weekend to check your basket of eggs.

Since coming home for a visit in late 2008, I’ve been trying to figure out how to help friends avoid such a large market drop again. I was living in Indonesia at the time and had no idea there was a major financial crisis happening. I had direct experience with the Asian financial crisis, but from a business experience, opening a restaurant, not from an investment of savings perspective.

It really bothered me that financial advisors that my friends trusted and relied on, didn’t help them avoid the big drop. I now see how difficult that can be. Imagine you and many other people have your RV parked in a lot, as many do. Suddenly there’s an amber alert for a hailstorm or tornado. If it was parked at your house and you had a ‘hail tarp’ in your garage, you could hurry out, throw it on and tie it down. There’s simply no way a single guy watching over the RV parking lot can do anything to protect all the RVs.

Most people have a range of investments and most financial advisors have many clients, all with different perspectives. It wouldn’t be easy to tell everybody they should sell. Not easy, but that’s what they needed to do late 2007, early 2020 and late 2021. That’s their job. If your advisor didn’t help you avoid those drops, I doubt they’ll help you avoid the next one. If you have full control, on your phone, you can take action at any moment to protect all your investments.

At that time, my brother had started trading with Questrade and was making 5% every 2 weeks buying and selling Suncor as it followed a steady wave up and down. Since I had no money, no job and a debt to pay off, from the restaurant and other failed efforts, I borrowed some money and went after the same 5% returns. I got one, then sold a second time, but it went higher, breaking the trend. After that, it was me chasing and selling as it dropped right after buying. Yeah, it was a nightmare, but I’m not one to back down from a challenge, and I could see the long term potential.

In 2009 and 2010, everyone seemed to be debating the issue of inflation or deflation. Both sides had compelling arguments. A lot of people were also touting gold and gold miners as the best investment. I didn’t know anything about anything, so I diligently read as much as I could and tried to figure out the ‘truth’. Long story short, I eventually whittled down the list of ‘experts’ who were even remotely correct, as proven by their results. Sadly, those few were eventually proven fallible as well.

In December, 2021, I was certain enough about my own ideas, that I felt compelled to write several articles, “Are You Ready For The Next Market Crash?”, before Christmas, and on Boxing Day, “Give The Gift Of Financial Security Next Year.”. I simply had to let people know that 2022 might see a large market drop.

In January, 2022, Seeking Alpha, where I was getting all my bad investment advice, dropped their blog feature and I switched to substack and wrote “Are you ready for the next market crash?”. That was a total of 4 articles over a 1 month period, suggesting a large market drop was coming and urging people to take action. Did your financial advisor contact you around that time and suggest you take action?

Since then, I’ve written many articles, sharing my ideas as I continued my quest to find a solution to my original concern. I’m happy to say, that the final piece to the puzzle was figured out in December, 2023. I was finally ready to share my ideas, with conviction, and I went on a bit of a writing binge. “Unraveling the mystery of investing.”, “Make 2024 a year of change!”, “$10k + 10min/wk +10yr = $1M”, and finally “TQQQ/HQU - Leverage can be a useful tool.” on Jan. 15.

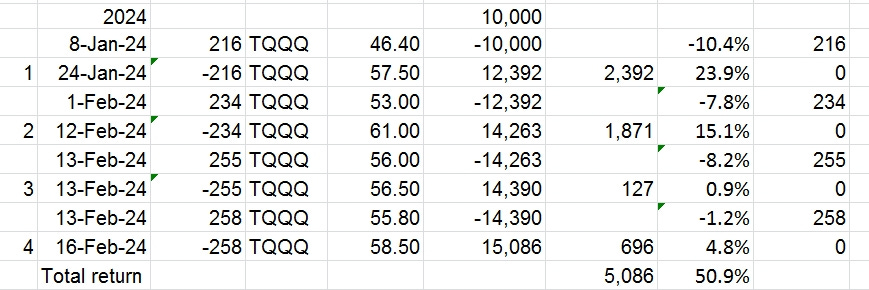

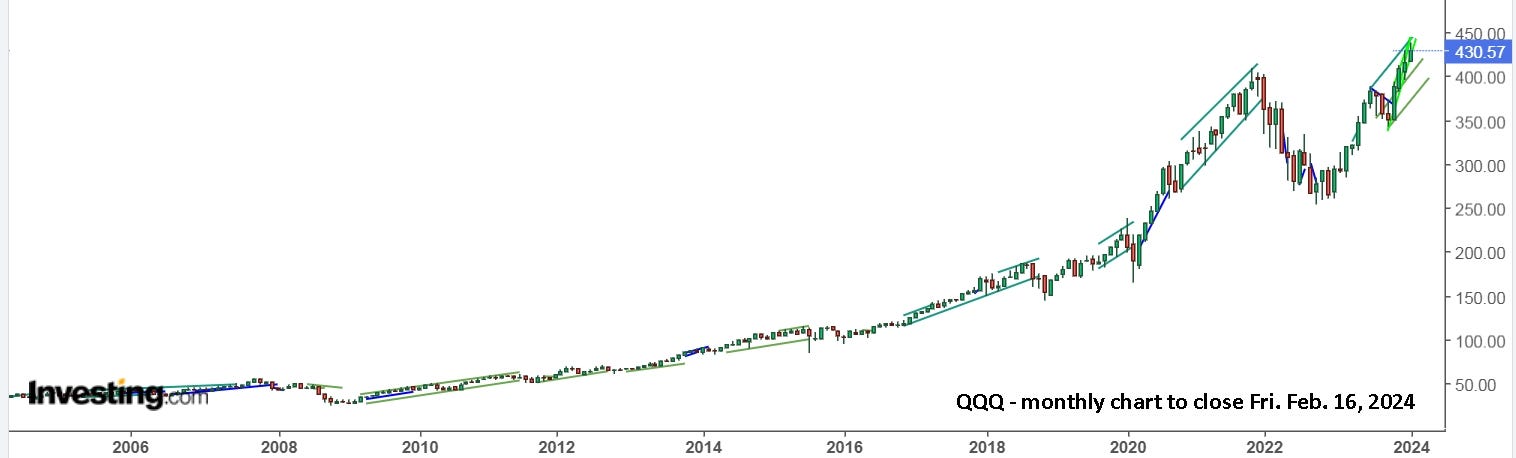

The first 3 articles laid out the plan with a lot of looking back in time to show how well it would have worked in the past. Anyone who agreed with the strategy bought TQQQ, a leveraged version of QQQ, which follows the Nasdaq, on Monday, January 8, when the markets gapped higher to open. Since then, with 4 trades, trusting the trendlines, you’re up 50%. If you simply bought Jan. 8 and are still holding, you’re up 23.7%, which is a nice return in 6 weeks. I prefer to make a bit of effort and get 50%.

The missing piece to my puzzle was not having the trendlines drawn on the active charts, so I could see, in real time, what was in my head from my weekend review. Without seeing the line on the chart on Jan. 17, you might logically and reasonably sell for a gain of 3.2% at the low, as it fell from the open. With the line visible, extending into the future, there’s absolutely no need for concern, and it in fact becomes a chance to buy more, or buy now if you missed the Jan. 8 buy.

Note also that the Jan. 8 buy was a 10.4% discount from selling Thursday, Dec. 28, which locked in a gain of 61.9% from buying Tuesday, Oct. 31. With it approaching the upper trendline on Jan. 24, it’s pretty obvious to be ready and waiting to sell and lock in a gain of 24%. On Feb. 1, it makes a higher low from the previous day, the trend is still up and you buy at 53.00 as it moves up from a low of 52.92. That’s 7.8% cheaper than you sold a few days ago and follows the strategy. Put in an alert and stop sell at 52.70 (-0.6%) and carry on with your day. It’s that simple.

Hopefully, you can see that it is already mathematically impossible for you to lose money going forward. You never hold for more than a 1-3% loss after buying, and you’re already up 23.9% from your first buy.

There are several factors that make this strategy so effective. First, all your eggs are in one basket. You only have one RV to protect. QQQ follows the Nasdaq, which gives you all the diversification you need. Holding QQQ allows you to hold shares in META, MSFT, AMZN, GOOG, NVDA, etc, but all within a single ETF that you can sell (and buy) at a moments notice. That’s why it’s so safe.

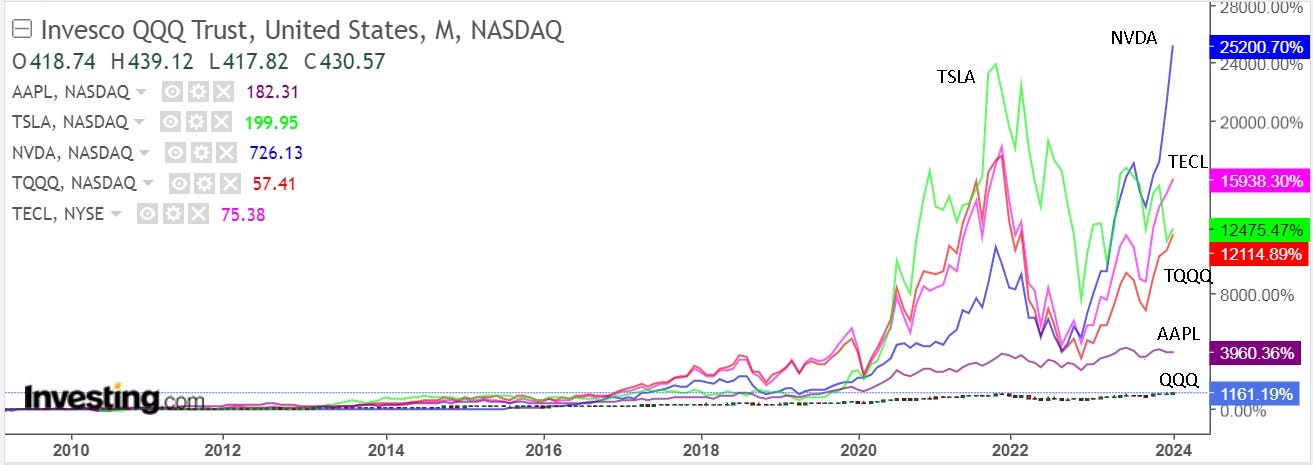

Second, and because you know it’s safe, trading the leveraged version, TQQQ, allows you to match the performance of the best individual stocks, like NVDA. That was a bit of a game changer for me. I wanted to ‘enjoy the ride’ with great picks like NVDA, TSLA, etc., and I did, to some extent, but it’s a lot of effort with a lot more risk. Here’s a look at simply buying and holding since April, 2009.

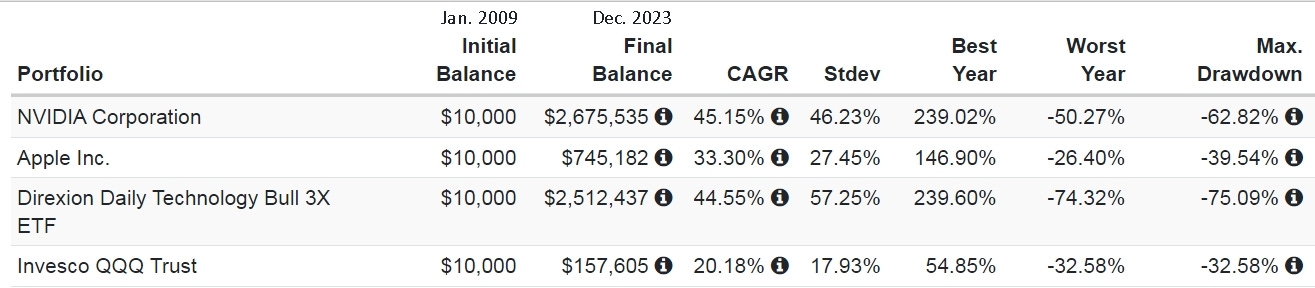

TSLA and NVDA had periods where they outperformed everything, and you can expect NVDA to have a fall like TSLA did. TECL is similar to TQQQ but follows XLK, which is more heavily focused on MSFT and AAPL (43% combined). Clearly, late 2021 was a good time to sell everything, and you now realize that was easy to do. And don’t forget that QQQ was a ‘good’ investment at 20.2% CAGR, turning $10k into $157k. For comparison, TD bank gave 13.9% CAGR, turning $10k into $70k. How did your portfolio do?

Buying NVDA on January 1, 2009 and holding through to December 31, 2023 turned $10k into an amazing $2.67M! TECL nearly matched it at 44.5% CAGR, turning $10k into $2.5M. And that’s doing nothing! Those monster returns include riding out the drops in 2018 and 2020. Imagine if you had stepped aside for those and others, which you now realize was easy to do.

That inspired an idea for an article, “$10k + 10min/wk +10yr = $1M”. From 2014 to 2023, holding QQQ turned $10k into $48.6k. Making just 7 trades in 10 years increased the return by 3x to $143k. That’s the potential with a bit of effort, just 10 minutes on the weekend. With TQQQ, 16 trades turned $10k into $44.3M. That’s definitely worth a bit of effort! And remember, I’m only telling people because I believe it’s absolutely possible.

So, forget about trying to pick the next big winner. Forget about AI. It will fade, just like 3D printing, solar, EVs, cannabis and all the other bubbles. Forget also about all value stocks and dividend stocks. Buying TQQQ and checking it once a week is by far the safest investment you can make.

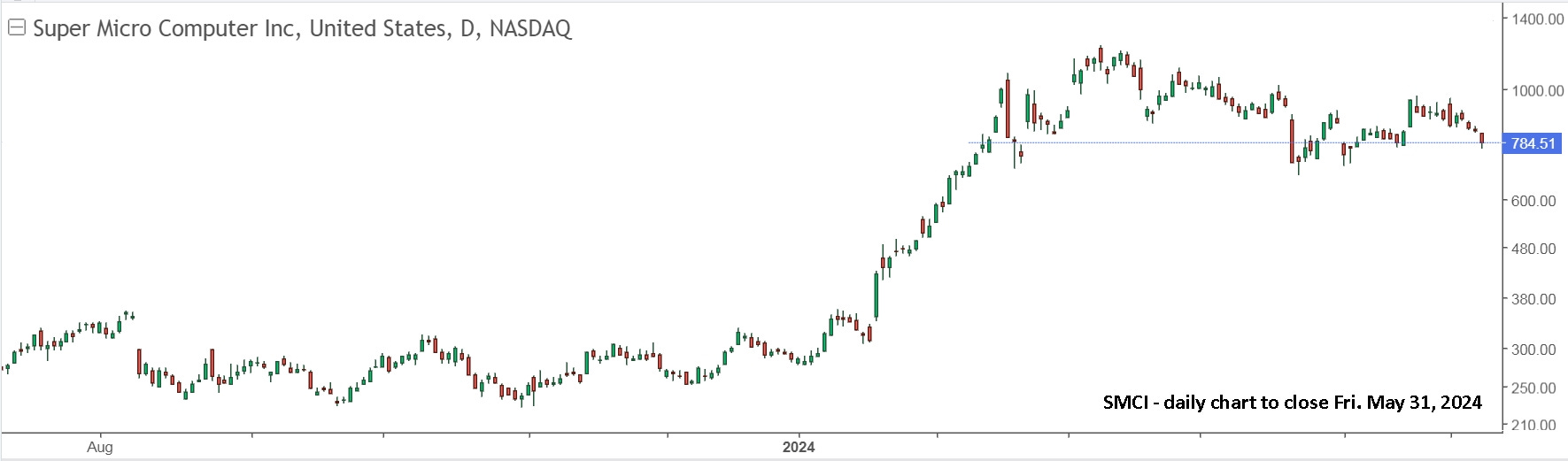

AI is the current fad and Nvidia is a great company, but its stock is way over valued, even if some financial experts say it isn’t and you should buy now. Another big winner in the fad is SMCI. On Feb. 5, a friend wrote “SMCI is off the charts, up 700% in year, yeah right. I decided to play a short on that one at $627.” I replied that it might go to 700+ or even 990, and later said it might top 1000. It hit 1006 on Thursday, so good thing my friend decided to close his short and take the small loss. It opened Friday at 1040.82, hit 1077.80 in the first 10 minutes, and with TQQQ falling from the open, I was pretty certain SMCI was ready to drop. It closed 803.32 (-19.99%).

You can be sure that many people are holding their high buys and buying more on this ‘gift’ to buy cheaper. Maybe it will go higher. I have no idea, but I don’t want to risk my money on it.

Update to Fri. May 31: SMCI did manage to make a new high, but it’s been essentially sideways over a wide range.

NVDA also finally topped 1000 and hit a high of 1157.58 early on Wednesday, May 29. That was a good time to take a swing short with NVDS, and you were watching for a top since Monday with it up against a weekly resistance line from Jan. 2018 and Nov. 2021.

I would definitely be taking the win with NVDA and taking my profit off the table.

A third key benefit of my new strategy is that it doesn’t try to predict what is going to happen. It simply shows the ‘lane’ going forward. It’s a lot like driving a car and simply staying on the road and not hitting the ditch. Here’s another look at TQQQ. Whenever it gets close to the upper resistance line, I’m ready and watching to sell.

In my Feb. 10 weekend update, I wrote “For me, if it gets near 62 on Monday, I will sell to avoid a possible gap lower on Tuesday following the CPI report.” It hit 61.14 at 11:35, then held a hard ceiling of 61 for nearly 2 hours. I sold at 61. When it gapped lower on Tuesday and moved up, I bought. When it reversed, I sold for a small gain. Then, when it held the support line and rallied late in the day, I bought. Without the line showing, there’s absolutely no reason to have bought. When it hit 59.13 off the open on Friday, matching Thursday’s high, and fell hard in the first minutes, you could have sold or put in a stop sell at 59.80 or 59.50 or whatever number you thought best. You’re now safely on the sidelines with all your original investment and 50% profit in 6 weeks. And remember, 44.5% CAGR, turns $10k into $2.5M in 10 years.

You might wonder why I sold Friday with it still above the light green support line. The hourly view doesn’t show how steep that line actually is. The markets are hitting new all time highs and are really due for a pullback. I’m not expecting a major market crash this year, but it could happen. Will you be ready if it does?

Update to Fri. May 31: I now use log scale on my charts to maintain perspective and remove the distortion of the above chart. Here’s a look at the current chart.

It’s at upper resistance and may continue up, like it did in 2021, but clearly it’s time for caution, with an exit plan ready and waiting to be executed.

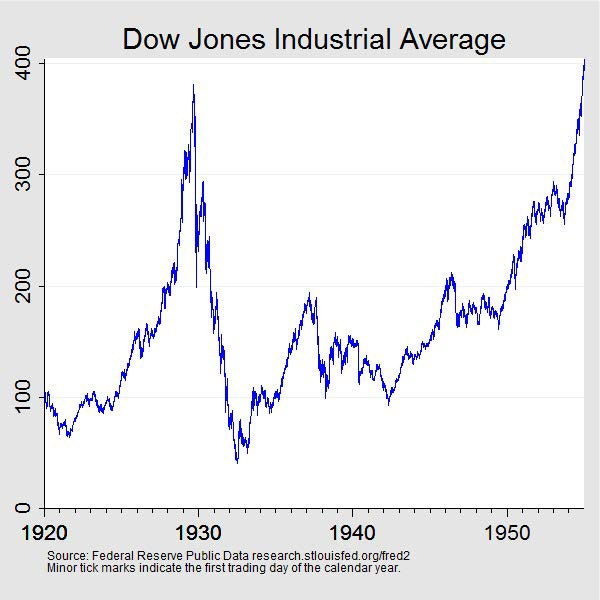

I went back in time and drew trendlines back to March, 1999. Then, looking at a weekly view, but not seeing the trendlines in advance, I asked Dad when he would buy and sell. It was remarkable and really helped clarify a few points. I repeated the exercise with 2 friends. Again, remarkable and enlightening. The effectiveness of the trendlines for the entire period since 1999 was undeniable. I then tried it with the S&P 500 since 1996. Same result. I also did it with TD and CAT. Equally effective.

Some financial analysts say we’re entering a period equivalent to the roaring twenties, with innovations that will spur the economy and markets for years. Others say that the party could end with a final high this year. Many others have been saying we’re in a bear market since early 2021. Best to ignore them. Regardless, we all know what happened after the roaring twenties. “On Black Monday, October 28, 1929, the Dow declined nearly 13 percent. On the following day, Black Tuesday, the market dropped nearly 12 percent. By mid-November, the Dow had lost almost half of its value.” If that happens again and you are in control, you sell on Monday for a loss of less than 5%. If your financial advisor is still in control, you will likely still be holding by mid-November and still holding a year later.

It took 25 years to get back to the same level. Clearly, you do not want to hang on to any of your investments when the markets take their next major tumble.

So, how do you protect your investments, and your RV? Take action. Take control and be prepared. It’s remarkably simple. Back in 2008, it wasn’t nearly as easy. Online trading was relatively new. Now, it’s common place. Personally, I recommend Wealthsimple for all Canadians. They’re the only platform that gives unlimited free trades. Questrade, which claims to be the No.1 online broker with low fees, charges $4.95 per trade. Banks charge around $10 with limited free trades for new accounts. Sure, give a discount to new accounts while continuing to rip off existing accounts.

You may think $10 is fair, but it’s a click of a button and free for virtually all platforms in the U.S.. Why not support Wealthsimple who isn’t wasting money on TV ads and is instead focusing on continually improving their product? They make money by charging a 1.5% exchange fee from CDN$ to USD, which the others also charge. Last year they began offering a premium account. For deposits over C$100k, you get free USD trades and 4.5% interest on the cash in your account. You simply pay a one time exchange fee in and out, which is indeed completely fair and reasonable.

If you have questions, please ask in the comments or contact me directly. I’d be happy to help. You can also show this to your financial advisor and ask their opinion. Many of you may be holding shares in Canadian banks, feeling it’s a safe investment with a good dividend. Here’s a a look at TD.

The trendlines would have had you safely on the sidelines in 2020 and 2022. Imagine making your annual or monthly purchase in January, 2022 at $100+. You’re still getting your 4% dividend, which is higher now, about 5%, but if you want your money, you only get 80 cents on the dollar. Now look again at 2020 and decide if you want to continue holding as it ranges in price from 76 to 86, and note that buying at 76 and selling at 86 is +13.2%. Far more than the annual dividend. You can also get 5% in a term deposit, or 4.5% with Wealthsimple and start managing your own money.

Update to Fri. May 31: TD has mostly held above 76 and there was a final opportunity in April to sell near 82, if you didn’t sell in March for more than 82, up to 82.50. If you’re still holding shares, the best choice is to sell. Yes, it might now be a bargain, but the risk is simply too great.

You might also be holding shares in Telus. You can draw your own lines on this chart and ask your financial advisor why the heck you have shares.

Update to Fri. May 31: Hopefully you took action the week after this article was posted.

Financial advisors will continue to suggest the need to stay invested, saying it’s impossible to ‘time the market’. Frankly, you’ve already seen how easy it is to avoid large market drops. I recently came across a ludicrous and widely touted ‘fact’ about missing the best days in the market. I felt compelled to have something on the internet that contradicts this idea. “Missing the Market’s Best Days is a Straw Man Argument.”

Some people are great coaches and others are great athletes. I was quarterback for one play in high school. Don’t ask how it went. I can’t remember why someone needed to fill in for that one play, and it was a simple hand-off, that turned into a fumble. I’m not great at investing either. I still find it difficult to make the right decisions at the moment. The active trendlines have been an enormous help. I am however, an excellent teacher and coach. Watching the Superbowl recently, it was very clear how important play calling and strategy is. Then it’s up to the players to execute it well. I’ll be your coach, if you want to be the quarterback of your financial future.

TQQQ hit 54.84 on a spike at 10:30 from 55.09. I bought the reversal and it rallied to 55.95 at 11:00 and fell back to 55.57, then held .60s and low .70s. When I looked at QQQ, I realized there was no real support line for it anywhere. The steep support line was touched Friday. They rallied for a few minutes from a gap open lower and then fell hard. Sell was the plan as was buying TQQQ near 55. As I thought more about QQQ, I decided to sell TQQQ on a stop at 55.50. I added new trendlines for QQQ yesterday but there's no strength yet to the upside, so best to remain on the sidelines and wait for some strength. I took UVXY for a trade yesterday and am in again today. I was early selling SOXS from Friday, but still got a decent gain and got gains with SOXL and TQQQ, so I'm content to have not fumbled the ball this time.

Based on TQQQ hourly chart, would you currently have a breakeven stop, or allow a retest of the dark green line at 55.00?